I’ve been trying to better understand the current economic crisis in Lebanon, and this post is my attempt to describe my understanding of the situation.

As a preface, I’ll note that my understanding has, for the most part, been mostly influenced by Toufic Gaspard (former advisor to Lebanese Minister of Finance) and Dan Azzi (former CEO of Standard Chartered Bank in Lebanon), as I found their (financial) arguments to be more convincing than their opposite counter-parts. Nassim Taleb (of Black Swan fame) seems to also be in broad agreement with them about the fundamentals (though they may differ on the details). I’ve provided several links at the bottom of the post to articles that helped me form my opinions.

Although the title of this post reads “Lebanon’s Currency Crisis”, Lebanon is actually going through multiple crises:

(1) A currency crisis (specifically a US Dollar crisis; I will use $ to refer to US Dollars going forward)

(2) A debt crisis

(3) An economic crisis (lack of jobs, economic contraction etc).

The focus of this post is on the currency crisis, although I plan on discussing the other crises in future posts. The crux of the currency crisis is this: Lebanon has been running a $ “Ponzi-like” scheme, which depends on a continuous flow of new $ entering the country from overseas to make good on old $ liabilities inside the country (for e.g. customer deposits at banks in $). When the inflow of fresh overseas $ significantly reduces over an extended period of time while liabilities in $ continue to grow (for e.g. because of increasingly generous interest on $ deposited, which compound over time), it becomes harder and harder to meet $ obligations over time. As such, when enough depositors start knocking on bank doors demanding the $ in their bank accounts and there aren’t enough physical $ (i.e. “real $”) to go around to meet all obligations – and importantly, your central bank can’t act as a lender of last resort by “printing” $ (i.e. Banque du Liban is not the Fed) – you have a currency crisis. This may all sound surreal or incomprehensible. To some extent, it is surreal, although I hope to make it less incomprehensible by working through the details in this post.

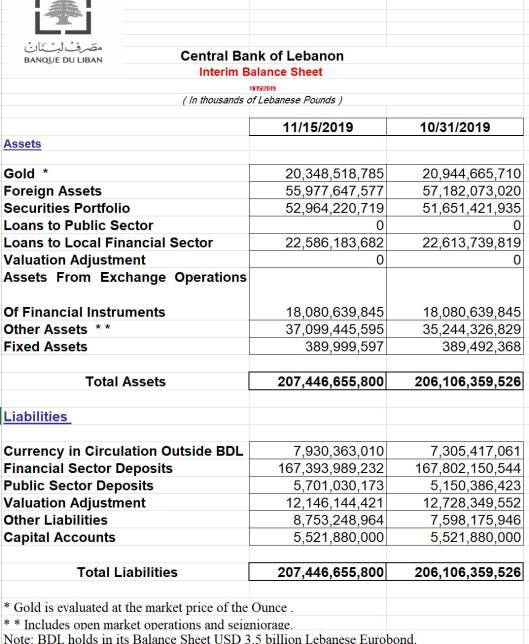

What is the evidence for the claim above? Answer: Banque du Liban’s (BDL) balance sheet. Indeed, it is highly likely that BDL’s $ liabilities significantly exceed its $ assets (based on educated estimates of $ assets and liabilities on its balance sheet, which doesn’t split Lebanese Lira (LL) from $). This means the difference between the two can be interpreted as “virtual $”, in the sense of not actually being backed by “real $” or actual physical $ (I call these “virtual $” and not “fake $”, in the sense that these $ can be transferred from one bank to another within Lebanon, but good luck moving these $ out of the country, as people outside of Lebanon want real “physical $”; Dan Azzi calls these virtual $ “Lebanese dollars”).

If you look at the Central Bank’s balance sheet, you’ll notice Foreign assets of ~LL 56 trillion (mostly cash $ and liquid US treasuries), and liabilities in the form of financial sector deposits of LL 167 trillion (important note: BDL reports everything in LL, even though those numbers include $; they simply use the official conversion of 1507.5 LL to $ when reporting their numbers on the balance sheet). Given the lack of LL vs $ split on the liabilities side, one has to make some assumptions on that LL vs $ split. The best estimate I’ve seen is that ~70% of those deposits are in $ (in fact, Riah Salameh himself mentioned a “dollarization” percentage of 70% on the BDL website). If we take that split, this means that there is ~$37 billion of physical $ on BDL’s balance sheet (excluding gold), and about ~$77 billion of liabilities in the form of deposits (i.e. LL 167 trillion / 1507.5 * 0.7). This means that there is a difference of 40 billion $ between foreign assets and liabilities (i.e. there is ~40 billion “virtual $”). Given that these $ deposits (on the liabilities side) are actually customer deposits that commercial banks have deposited at the Central Bank (we’ll talk about that below), if you follow this logic to its bitter end, this implies that people’s $ accounts in their banks aren’t fully backed by real physical US $ (although some portion is, of course).

Now for people familiar with fractional reserve banking, this is not a big deal, right? Afterall, every bank in the world operates in similar fashion. That is true. Except for one very important difference: their centrals banks own the currency! BDL cannot act as a $ lender of last resort because it can’t print physical $, which means if everyone wanted to withdraw their $ at the same time, banks could not possibly give everyone their full $ deposits (which is why you keep on hearing from the corrupt political class that all is fine as long as you don’t withdraw your $ from your bank accounts). I should mention that the aforementioned is partially mitigated by the fact that many $ deposits are “frozen” in longer-term deals (so 1 or 3 or 5 year deals where $ cannot be withdrawn if the accounts are to receive the generous interest rates from the banks), but this doesn’t change the basic “virtual $” math (but does have an impact on available liquidity).

How did we get into this mess?

It’s essential to understand that the Lebanese system is entirely reliant on fresh $ flowing into the country from overseas (via remittances, investments, tourism and so on) in order for the system to “work”. When the inflow of these $ decreases, big problems arise, because of 3 reasons:

(a) The structural trade imbalance that Lebanon carries, with imports significantly exceeding exports

(b) The interest (and principle) paid to people outside of Lebanon on foreign-currency denominated debt (like Eurobonds, which unlike the name implies, are typically $ denominated)

(c) The desire by the Central Bank to maintain the official peg of the LL to the $, which has officially been pegged at 1507.5 LL to 1 $ (I believe that the band is actually between 1500 and 1515).

The trade imbalance is a result of Lebanon importing much more than it exports, which results in significant $ exiting the country (the most recent numbers suggest a trade imbalance of negative $14 to $15 billion). Why? Imports are typically paid in $ (i.e. importers must pay suppliers in $, especially for fuel, wheat and medicine), so importers who get paid locally in LL for their imported goods have to convert their LL into $, which they use to import those goods (resulting in an outflow of $ outside the country). Exports are typically in LL, which means overseas buyers must convert their $ into LL to purchase these exports (resulting in a new inflow of $). If the trade balance is negative, then more $ exit the country than $ enter the country (i.e. there is a net outflow of $ out of the country), which means new $ need to be sourced from outside the country in order for Lebanon to continue carrying a structural trade imbalance.

Foreign-denominated debt (such as Eurobonds) is issued by Lebanon in exchange for foreign currency (typically $), which (temporarily) increases $ reserves. Although most of this debt is owned by Lebanese banks, some portion of it is owned by people outside of Lebanon, which implies that the interest paid to them in $ exits the country and decreases $ reserves. Regarding the capital that needs to be paid back at maturity, typically, governments will issue new debt to pay for old debt, thus netting that out. It should, however, be mentioned that if the market believes that the country will default (which would be reflected by very high interest rates on any new bond offering), then the Lebanese government will be reluctant to issue new Eurobonds because it would not be willing to pay the extremely high interest on them; this means the country is essentially “locked out” of capital markets. In that scenario, the government will then also have to pay back the capital on maturing bonds from their $ reserves since it can’t issue new bonds to pay for maturing bonds, thus causing additional $ to leave the country to meet those maturing Eurobonds held by foreigners.

Finally, and importantly, the Central Bank in Lebanon has made it its primary missions to protect the peg at all costs. In order to do so, it needs to maintain a significant $ reserve to use when events necessitate either buying $ (and selling LL) or selling $ (and buying LL). So, for example, in the case of a “negative event” where people scramble to convert LL to $, this increases demand for $, and decreases demand for LL, which should theoretically strengthen the $ against the LL if the currency was floated. However, the currency is pegged, and to maintain the peg, the Central Bank has to buy up LL and sell $, which means this operation is costing the Central Bank precious $ that reduce its $ reserves (note that the Central Bank does not publish the $ cost of such operations, but it needs to replenish its $ reserves after such negative events).

Where do these replenishing $ come from? Ultimately, they come from outside the country of course, since the Lebanese Central Bank can’t physically print $. The main outside source of these $ are investments, tourism, and remittances from the Lebanese diaspora (in 2008, remittances alone were an insane ~25% of GDP). Now in 2016, mostly because of the oil crisis in the Gulf (and the Yemen war), Gulf countries’ finances got hit hard and they started restructuring their economies, and remittances started to decrease into Lebanon as Lebanese expats living in Saudi, UAE etc lost their jobs or weren’t being paid (I’ve seen numbers suggesting that nearly half of remittances into Lebanon come from the GCC). This trend over the past several years has only worsened, and the numbers this year suggest that remittances will likely total only a couple of billion $ (far lower than historical averages).

Of course, the other two sources of $ inflows (investments and tourism) have also been hit for several years in a row, mostly because of the geo-political situation in the region (the Syria war and decisions by Gulf countries to limit tourism to Lebanon because of security and political reasons).

With $ inflows reducing over time, the Central Bank started getting desperate as it needed to attract fresh $ to continue maintaining the peg and the country needed $ to plug the large trade imbalance. So in 2016, it engaged in the infamous financial engineering operations that have rightfully received much criticism. Without getting into details, the Central Bank essentially offered up massive returns (in LL) to commercial banks to deposit their customers’ $ at the Central Bank (I’ve seen estimates of 17% return or higher offered by the Central Bank to commercial banks). This incentivized commercial banks to increase $ interest on $ deposits to attract additional $ so that they could deposit those new $ at the Central Bank to earn that high interest (the interest on $ deposits at commercial banks would of course be set at less than the interest they would receive from the Central bank, with the delta being bank profit). These deposited $ would then be used by the Central Bank to continue protecting the peg, paying $ denominated debt and ultimately, plugging the trade imbalance. Commercial banks made lots of money, and depositors were receiving very high $ interest on their $ deposits. Everyone should be happy, right? Wrong. Unless you can print physical $, the amount of physical $ in the country is entirely dependent on the existing $ reserves in the country plus the physical $ inflow minus the physical $ outflow. So although the accounts, on paper, were increasing in $ value because of the generous interest being paid on them, they weren’t entirely backed by equivalent physical $ because the rate of increase of $ in accounts was higher than fresh physical $ net inflow. With higher and higher interests needed over time to continue attracting fresh $ from overseas, and lower and lower amounts of fresh $ making their way into Lebanon because of the aforementioned reasons, the amount of “virtual $” continued to grow over time. And when enough people started demanding their $, there simply wasn’t enough physical $ to go around, thus the $ currency crisis.

Some references that I found useful:

- Toufic Gaspard’s 2017 paper, which in retrospect, seems prophetic

- Toufic Gaspard’s 2019 update

- Fitch report that downgraded Lebanon’s credit rating even further

Several articles by Dan Azzi:

- Lebanon’s Richest Need To Take a Haircut

- What’s next for the Lebanese banking sector?

- Ye shall know the truth and the truth shall set you free

- What is to be done

- The devaluation of the Lebanese Dollar

- Zugzwang

- Dollars, the latest Lebanese vegetable

- Lebanon’s rentier economy and Creative Destruction

Other articles:

- Capital controls, devaluation, taxes

- Templeton Sees Lebanon on Road to Debt Default as Crisis Rages

- Les conditions de la communauté internationale pour sauver le Liban de la faillite

- Lebanon’s economy has long been sluggish. Now a crisis looms

- Breakdown of trust in financial system deepens crisis in Lebanon

- The Diaspora, Debt, and Dollarization